Is 'financial literacy' something we should teach?

Calls for more financial education are understandable. But adding curriculum descriptors isn't the answer.

Australia has developed a recent habit of going through prime ministers quickly, and many of them don’t cover themselves in glory after leaving office. The UK has also developed this bad habit. Which is why it is nice to see a former Prime Minister of the United Kingdom, at least, decide to do something useful in post-parliamentary life.

In 2025 Rishi Sunak and his wife, Akshata Murthy, founded the Richmond Project “to focus national attention on transforming lives by numbers, and to build greater number confidence.”1

Pleasingly, a vanity project this is not. A recent report was based on a survey of over 10,000 adults in Great Britain, specifically inquiring into their financial literacy: how many possessed the knowledge and awareness to make sound financial decisions. The researchers used a set of questions known as the ‘Big 3’, which test understanding of compound interest, inflation, and risk diversification. Here are some of its key findings:

Almost forty percent of British adults have poor financial literacy.

There is a socio-economic gradient, with those of higher socio-economic status outperforming less advantaged peers.

There is a strong gender gap, which men outperforming women within each social grade.

Older adults, even those with a GCSE (Year 10-equivalent) education outperform younger people, even those with a postgraduate degree.

The most important finding for educators and education policy people, in my view, is the way the report states the obvious: poor financial literacy is linked to poor numeracy. As Sunak himself commented at the report’s release, “[t]oo many people are navigating saving, borrowing and planning for the future without the confidence or knowledge they need, and many associate numbers with anxiety rather than opportunity.”

Forget the appeals to employability that usually accompany demands to change what students are taught and, for a moment, reflect on the real-world implications. A sound knowledge of basic financial concepts is the difference between making wise decisions around everyday tasks in adult life, like where and how to save your money, how to plan for retirement, and what the implications of interest rates are for decisions like car or home loans. Understanding the basic concepts such as those tested in the ‘Big Three’ should be part of the knowledge-rich curriculum.

Often the response is just to ‘add it to the curriculum’, and indeed that is what is happening here, with Richmond’s report endorsing the government’s decision to add financial education into primary school lessons, part and parcel of the recent curriculum review. According to Education Endowment Foundation head Becky Francis, who led the curriculum review process, “financial literacy was the most highlighted area of importance by parents and the one topic that was consistently raised by every single focus group with young people”.

Australia is no different

Late last year, Australia’s Education Minister Jason Clare announced a ‘keyhole surgery’ refresh of the F-2 Australian Curriculum for Mathematics. Very little is publicly available about that process. But one thing we do know, and that is there will be more consumer and financial literacy earlier in primary school.2

In remarks to the Sydney Morning Herald’s annual Schools Summit, ACARA chief Stephen Gniel made the following comments:

It’s a refinement of the Maths curriculum. The aim is clear.

Provide advice on the prioritisation of content and greater mathematical details to improve clarity for teachers about what students will learn.

Set out specific sequencing of content, highlighting related concepts and the sequence of introducing concepts.

And ensure the inclusion of explicit content on foundational consumer and financial literacy.

Think of it as keyhole rather than open-heart surgery.

In additional comments to the Sydney Morning Herald, Gniel said “[Financial literacy] is another one that comes up all the time. We must prepare our children for their responsibilities and also the tricks of the trade around financial and consumer and financial literacy.”

That doesn’t tell us a great deal about what is going to change, and it will be a matter of wait and see. But, like Francis, Gniel is saying financial literacy is one that is commonly raised. It would be rare to find disagreement that part of educating students for the real world means giving them a basic, consumer-level understanding of finance.

But there is a lot that could potentially fall under the label ‘financial literacy’, necessitating clarity on what exactly it is and how this sits within the current curriculum. What do we really know about Australians’ knowledge of financial literacy, and how does this compare internationally? Even though everyone already cares a lot about financial literacy, is adding another ingredient into the curriculum soup the best solution?

Financial literacy, and assessing it via the ‘Big 3’

Helpfully, the Victorian Department of Education’s Policy and Advisory Library contains some clear definitions of financial literacy:

Financial literacy is defined by the world’s Organisation for Economic Co-operation and Development (OECD) as a combination of financial awareness, knowledge, skills, attitudes and behaviours necessary to make sound financial decisions and achieve individual financial well-being.

The Victorian Curriculum and Assessment Authority (VCAA) defines financial literacy as ‘the ability to understand and apply different financial skills effectively, including personal financial management, managing debt, investing, budgeting and saving.’

Interestingly the OECD definition includes behaviours as well as knowledge, skills and attitudes, although I am unsure how one would go about measuring said behaviours. The VCAA definition is a little bit more specific about what financial skills it is looking for, naming debt, investing, budgeting and saving, all within a personal finance context. This makes sense to me, but it’s worth acknowledging there are different definitions.

Annamaria Lusardi and Olivia S. Mitchell are the inventors of the ‘Big 3’ and have carried out extensive international research on financial literacy, arguing the global shift away from defined benefit pension schemes linked to a job or a fixed government payment and towards contributory models provides a strong impetus for a closer look at this topic.3

[T]he new financial era imposes a much heavier burden on workers and their households to become financially literate – to learn how to process economic information and make informed decisions about household finances.

Accordingly, they assessed interest compounding, inflation, and risk diversification using these three questions:

In Australia

Australia’s Household Income and Labour Dynamics in Australia (HILDA) survey is a large, longitudinal and representative survey of Australian households. The 2016 collection of HILDA included variants of the Lusardi and Mitchell questions, asking participants the following:

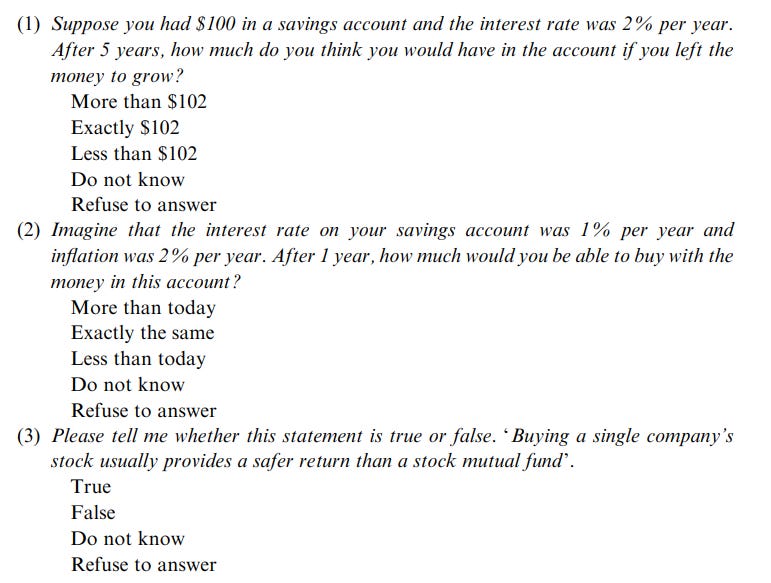

Q1: Interest Rate: “Suppose you put $100 into a no-fee savings account with a guaranteed interest rate of 2% per year. You don’t make any further payments into this account and you don’t withdraw any money. How much would be in the account at the end of the first year, once the interest payment is made?”

Q2: Inflation: “Imagine now that the interest rate on your savings account was 1% per year and inflation was 2% per year. After one year, would you be able to buy more than today, exactly the same as today, or less than today with the money in this account?”

Q3: Diversification: “Buying shares in a single company usually provides a safer return than buying shares in a number of different companies.” [True, False]

Q4: Risk: “An investment with a high return is likely to be high risk.” [True, False]

Q5: Money Illusion: “Suppose that by the year 2020 your income has doubled, but the prices of all of the things you buy have also doubled. In 2020, will you be able to buy more than today, exactly the same as today, or less than today with your income?”

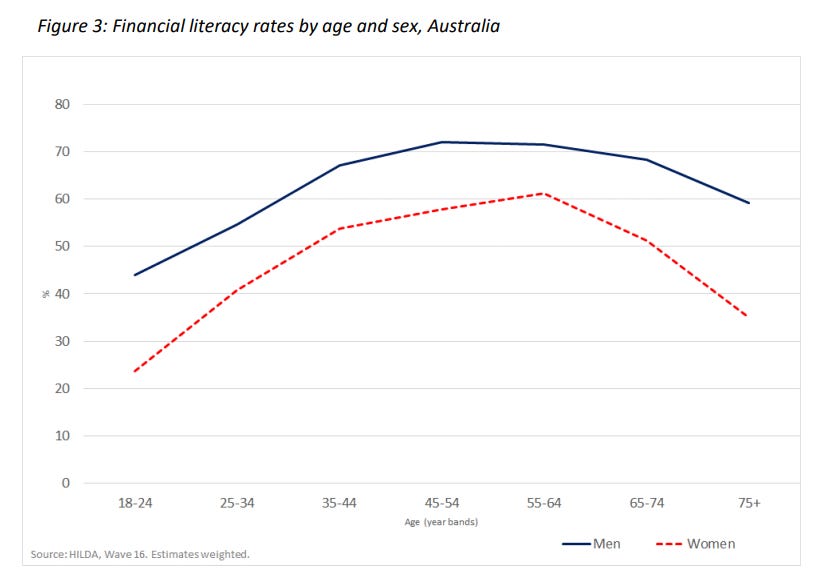

Analysis of the HILDA survey results by Alison Preston of the UWA Business School in March 2020 showed that when questions 1-3 (‘the big 3’) were used, 55% of adult Australians were financially literate. But this conceals a significant gap by gender: 63% of men, and only 48% of women. Financial literacy peaks when people are aged in their 50s, but the gap persists at all ages.4 The general shape and texture of these Australian results look quite similar to Richmond’s findings.

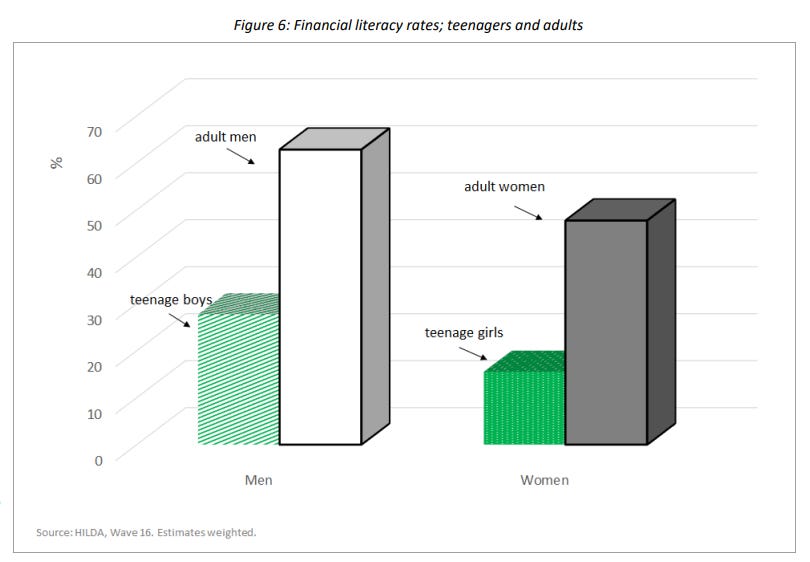

Preston’s analysis of HILDA includes teenagers 15-17 and shows that the gender gap evident in those 18-24 gap exists even for those on the cusp of adulthood: 28% of teenage males and 15% of teenage females were able to correctly answer the Big 3.

Commenting on the results overall, Preston argued:

Within and across Australia there is widespread financial illiteracy. Nationally one in three adult men and one in two adult women do not understand key basic financial literacy concepts such as interest rates, inflation and risk diversification. These are concerning shares, particularly in the context of rising household debt, increased individual responsibility for saving for retirement and easy access to credit.

In other countries

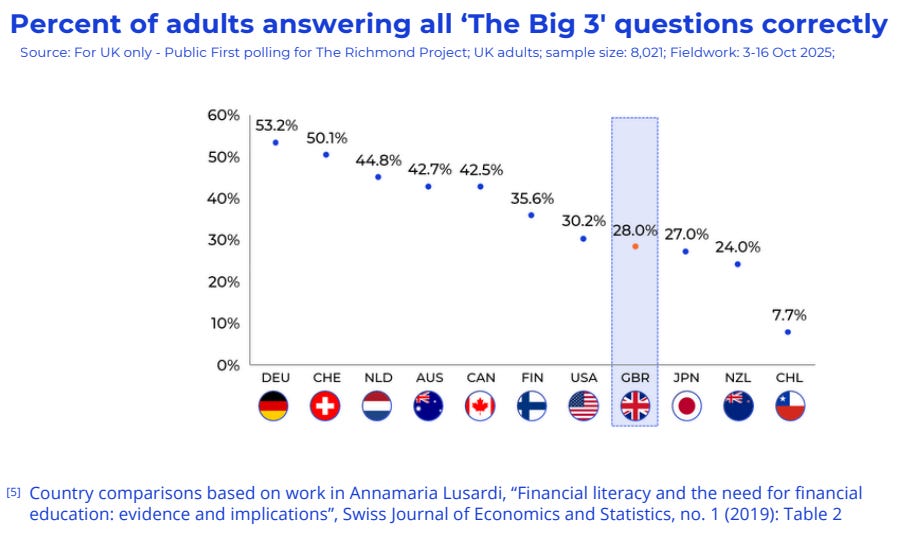

The Richmond Project report produced the below graphic which relies on a table of studies from a range of authors covering a range of different countries; Australia’s data is from a 2013 study with data from 2012. Without deep knowledge of sample construction it’s not possible to say whether the HILDA data above, from 2016, represents an ‘improvement’ for Australia.

Teaching financial literacy

Lusardi and Mitchell’s work is motivated by the idea that the relevance of financial literacy to the world of the average person has increased due to policy decisions. In other words, because we have built institutions, particularly around retirement savings, that require ordinary citizens to make increasingly sophisticated financial decisions, that creates a moral and ethical case for developing the knowledge base.

This is certainly the case in Australia, where the advent of compulsory superannuation has meant the creation of a significant financial asset, effectively quarantined for use in Australians’ retirement under strict rules, within a changing but still tax-advantaged policy landscape. For non-homeowners, superannuation is likely the largest asset they will ever have, and for homeowners it is probably second.

Even though superannuation is compulsory, there are good reasons for Australians to develop a better understanding of it. Agnew et al, who wrote the 2013 paper referenced in the Richmond Project graphic,5 offer the following:

[Australians] are responsible for decisions relating to the plan in which superannuation savings are managed and accumulate (including whether to create their own “self-managed superannuation fund” [SMSF] plan), for plan management (such as consolidation of multiple plans), for choice of investments (from increasingly long menus of single- and multi-manager diversified and single options, and often individual asset classes), for whether to make or increase voluntary contributions (for which the tax rules differ by type and contribution amount), for whether to seek and use financial advice, and for which benefit(s) to take at retirement. These decisions can be overwhelming.

A 2022 report from Griffith University academics Laura de Zwaan and Tracey West sought to understand more about what and how students learn about financial literacy concepts. Their study involved ‘inductive’ research across four Queensland government schools, conducting focus groups (n=16) and interviews (n=31). No quantitative survey such as the Big 3 was used.

They found the main source for students learning about money was their parents, followed by maths. Accounting and Business subjects also featured, but as these are electives this suggests the average student is learning about financial literacy in maths if at all. The authors found “[t]hroughout all four schools, students who were studying business had much broader and more detailed knowledge of financial concepts. Business studies helped some students learn about, or at least become aware of, concepts such as investing in shares, insurance and superannuation.”

This could represent a causal link - studying business leads to better knowledge - but could also indicate selection effects, as parents and students who value this type of knowledge are more likely to select business and accounting-related electives. In any case it does suggest leaving this material to electives only is unlikely to assist in the goal of broader financial literacy. That means we should look to the core, compulsory curriculum for years F-10.

Just put it in Maths?

De Zwaan and West found “[s]ome students clearly recalled learning about interest rates, compound interest and depreciation in Maths, while others only had vague recollections of learning about these financial concepts. Different assignments were mentioned, indicating that making learning about financial concepts assessable helps kids to retain this knowledge.”

To go back to the Big 3 questions, answering them requires some basic mathematical competence (percentages, rates, growth), but in order to apply the maths correctly, one requires understanding of specialised vocabulary such as:

Savings/savings account

Interest/interest rate

Inflation

Share/shares

Company

The Australian Curriculum website has a handy set of webpages for ‘consumer and financial literacy’ which enable you to see how this topic is integrated across curriculum areas for different year levels.

But if you spend any length of time on these webpages, you will quickly realise that most of these target vocabulary words do not exist in the (compulsory) curriculum descriptors, they exist only in the elaborations.

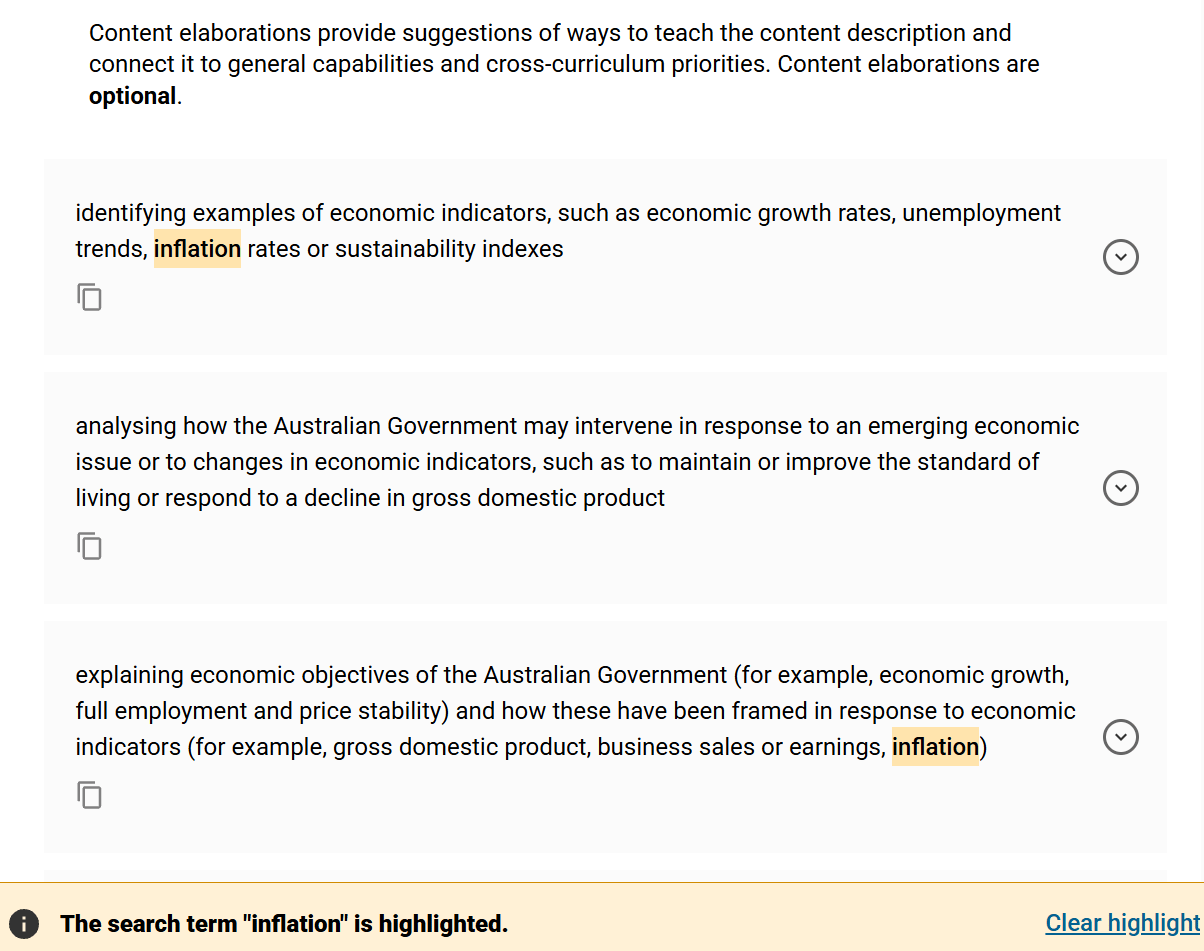

Let’s look more closely at ‘inflation’, which is a hinge concept in Question 2 of the Big 3.

Under Year 10 Economics and Business, I found this descriptor:

And then this under its elaborations:

So it’s not surprising that inflation - a real ‘hinge’ concept in Question 2 of the Big 3 - was something De Zwaan and West found students did not understand when they put this question to their research participants:

There was very little knowledge of inflation and most students had never heard of it before. One teacher suggested they may be aware of it as Consumer Price Index (CPI), but when we tried that approach, students did not recognise that term either.

The inflation finding is important as Lusardi and Mitchell’s ‘Big 3’ financial literacy questions, often used to measure financial literacy, contain a question on inflation. If students do not know or understand what inflation is, they will not be able to answer this question correctly. It is also important to understand that if a person’s wage does not increase in line with inflation, then that person’s purchasing power is eroded over time. As students are making decisions on career and lifestyle pathways, insights into the importance of wage growth can help make informed decisions.

The interviewers asked students what was going through their brain when shown Question 2 of the Big 3:

“ I think I learnt this last year. Is it like the interest rate, and the P. I forgot what the P meant.”

‘ Math.’

On the latter student, the report states “She froze and couldn’t really consider the question because the Maths was standing in the way. She was trying to recall formulas rather than just trying to understand the question.”

As the report correctly notes, “The most interesting part of this reaction from the students is that the question does not require a calculation to be able to answer it. As long as they understand the financial concept, they can answer it quite easily” (my emphasis here).

This suggests at least one of the following is happening: a) students’ emotions about Maths, rather than actual capability, is a hurdle which stops them from recognising the underlying financial concept and/or b) they simply do not understand the financial concept well enough to see that the maths is not relevant. I’m willing to bet it’s both for some students, and at least b) for most.

A curriculum quantity issue, or a curriculum quality issue?

It would take more time and resources than I currently have to go through the consumer and financial literacy-linked curriculum content with a fine-toothed comb to unpack whether the issue is quantity or quality. From a brief scan, I suspect it is both: there is not enough in the written curriculum that would result in a student, with no other access to this knowledge, developing the sort of capacity that enables them to answer questions like the Big 3 accurately. This makes it an equity issue.

But let’s imagine for a moment the Australian Curriculum and its variants amounted to an excellent written curriculum. The reality is that with school-level flexibility about the implementation will mean a significant amount of variation in the enacted curriculum. Most teachers and teaching teams naturally gravitate towards teaching the strands of the Humanities curriculum they feel most comfortable with. Given most Humanities teachers have, like me, some combination of a history and politics background, the order of priority for the four strands typically looks something like this:

History

Daylight

Civics and citizenship

Geography

Economics and business

It is the Economics and Business strand of Humanities which, aside from the odd consumer arithmetic element in Maths, contains the majority of relevant content. Economics and business is in itself fairly broad. It contains everything from ideas of business creation and entrepreneurship, to business/economic cycles (ideas like recession, growth, GDP), and personal and consumer-related concepts.

But I do wonder how much of it is actually taught, how well, and to how many students. New South Wales, for instance, has a Commerce elective available for Years 9 and 10. Perhaps their knowledge-rich syllabus is a ‘best in class’ for this topic. Victorian schools tend to offer electives for Year 10 that align with VCE subjects; Business Management, Accounting and Economics are separate subjects. How many teachers of these specialist electives for Years 9 and up are involved in writing the economics and business units of the Humanities curriculum for Year 8 and below? How many schools are even running these electives at intermediate years full stop?

I don’t know what the solution is here, or how one would make space for making the fundamentals of personal consumer and financial literacy a knowledge entitlement - and therefore part of the non-elective curriculum - for students. But I would tentatively suggest that another curriculum sprinkle is not the way forward. The first step should be to define what we would expect students to know in this area - which is more ‘applied knowledge’ than a discipline in its own right - and then see how well that is reflected in what is written down.

Please share your thoughts and experiences below, especially if you are a Humanities or Commerce teacher. I’d love to get feedback on this analysis and anything I have missed.

They named it after Richmond in North Yorkshire where they live, which - as I have just discovered - is basically the setting of Downton Abbey. If you look on a map you can see the towns of Ripon and Thirsk, which are mentioned on the show.

Annamaria Lusardi and Olivia S. Mitchell (2011). Financial literacy around the world: an overview. Journal of Pension Economics and Finance, 10, pp 497-508 doi:10.1017/ S1474747211000448

Julie R. Agnew, Hazel Bateman, and Susan Thorp. "Financial Literacy and Retirement Planning in Australia." Numeracy 6, Iss. 2 (2013): Article 7. DOI: http://dx.doi.org/10.5038/1936-4660.6.2.7

It has always seemed crazy to me when I teach my niche VCE subject of Economics that for many students it is the first time they ever come across concepts such as inflation or interest rates in their academic career.

Not to mention even further to that when we get into the weeds on tax brackets, the tax mix etc all of which currently impacts many of them with casual and part time jobs yet no understanding at all of what the numbers on their payslip mean.

It’s really not setting them up for success when they set off into the adult world when so many students could miss these in their education completely.

Clare’s keyhole surgery to the F-2 maths curriculum is a direct response to the Year 3 NAPLAN results.

It seems the specific addressing of financial literacy is not necessarily a part of that but rather a response to concerns for people’s financial literacy and therefore their happiness later in life.

If we can simply get our early number knowledge taught effectively in F-2 I can see the entire landscape changing for maths curriculum conversations and how we address financial literacy.

Like interest, better knowledge from the start has a compounding effect.

Financial literacy outcomes will improve dramatically simply because we have effectively taught our youngest how to unitise and regroup from the first years of schooling.

The implications of those simple skills being learnt properly early are much bigger that we are giving them credit.